Business Society: April Engineering Plastics Long Short Game: Half Up And Half Down, Difficult To Change

May 10, 2023

Leave a message

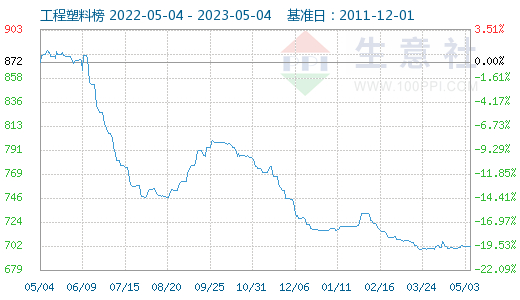

In April, the fundamental pattern of various products in the engineering plastic industry was different, reflecting a clear differentiation in price trends. In addition to PCs, POM has also joined the ranks of high load and low consumption this month, and the market is deeply constrained by supply and demand contradictions.

PET and PA6 were boosted by multiple factors and overall fluctuated and rose. On the other hand, the profitability of engineering plastic production enterprises is still facing challenges, and there is little improvement in the operational risks of factories at all levels. The combination of international oil prices rising first and then falling this month has weakened the common remote costs of the plastic industry. Overall, the engineering plastic industry showed a mixed performance in April, with the market playing a game.

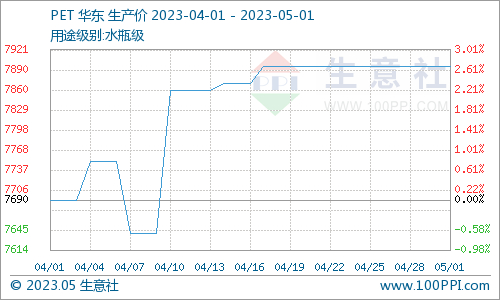

The price of PET water bottles was slightly stronger throughout April. The overall supply in the domestic market is tight, and downstream procurement is on demand, with a positive negotiation atmosphere. In the first ten days, there was strong support for the raw material end, driving the focus of negotiations in the PET market upward, while the overall cost end remained stable in the second half of the month.

PET manufacturers and merchants shipped normally within the month, with smooth logistics, and their offers increased by 2.68% compared to the same period last month. It is expected that the PET market may experience volatility and consolidation in the short term.

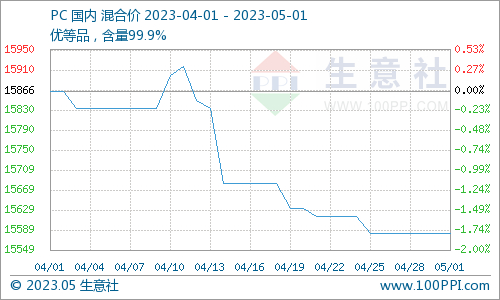

The domestic PC market in April continued the negative trend of the previous month, with prices fluctuating and falling. Within the month, the overall operating rate of domestic PCs was adjusted and operated in the range of around 70%, and the industry is still at a three-year high load with abundant supply. In addition, some maintenance plans have been delayed and new devices have been put into operation within the month. Overall, the positive impact of April’s negative reduction on the market has been smoothed out, and the expected increase in inventory and supply in the later period has resulted in poor support for spot goods.

Downstream buyers just need to maintain production, and operators have a more wait-and-see mentality. The auction situation also fell short of expectations. At present, the starting position of terminal enterprises is not high, and the actual stocking operation has not improved, with light on-site trading. Traders’ mentality has weakened. It is expected that the PC market will take some time to overcome the supply-demand contradiction and may continue to operate in a weak position.

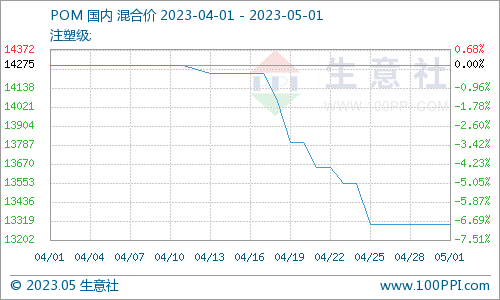

In April, the POM market remained stagnant in the first half of the month and declined in the second half. The operating rate of domestic polymerization plants has been adjusted to a high level, with an average monthly operating rate of 90.18%. The total monthly output is 35100 tons, and the industry’s inventory pressure is expanding. The demand side enterprises just need to replenish less, and some downstream operating rates are low, resulting in few actual transactions. Before and after the holiday, the market participation of practitioners decreased, terminal factories ceased production, and the stagnation of on-site supply intensified. Based on various bearish and bearish factors, it is predicted that the POM market in early May may mainly remain stable and wait and see the market trend

Future Market Forecast

In April, the prices of the five types of engineering plastics mentioned above rose, fell, and leveled, with roughly half the gains and losses on the surface, but in reality, the industry market is weak and difficult to improve. It is not difficult to see from the horizontal comparison of the ups and downs of various products that the industry generally tends to be weak. During the month, the pricing of aggregation enterprises is cautious, and it is common to lower the factory price in order to remove inventory. The stocking of end enterprises is concentrated in the range of low-end goods sources, and the demand is generally not high.

At the same time, after the international crude oil price rose this month, it fell deeply, and the support for the engineering plastics common remote raw materials failed to recover, but instead precooled. In addition, the macroeconomic environment is not providing enough support to the engineering plastic industry. Therefore, the Commodity Market Analysis System of the Business Society believes that the current market momentum improvement is limited, and the industry has a heavy wait-and-see mentality. It is expected that the overall market situation of the engineering plastic market in early May may turn into a bearish trend.

Completed The Belarusian Customer Order And Prepared For Shipment

Previous

Polypropylene And Other Plastic Products Will Be Reduced By 15% in Price! International Oil Prices Plummet, Domestic Chemical Prices Lose Cost Support

Next